Central Bank Digital Currency

Over the last decade, there has been a rapid acceleration in how we process information with cloud computing, artificial intelligence, and big data. Applications like Zoom and Twitter have us connected more than ever before, yet the process for sending and receiving money has fallen far behind. Financial institutions across the globe still rely on the Society for Worldwide Interbank Financial Telecommunication (SWIFT) banking system, developed in the early 1970s, to deliver cross-border payments between people, corporations, and banks. This once sophisticated system continues to send payment orders through financial networks that we are ready to outgrow. By digitalizing our dollar with Central Bank Digital Currency (CBDC), we can employ contemporary financial technology to find a novel approach to monetary transactions. Although CBDCs will present many technological and political challenges, they have the potential to improve payment efficiencies and strengthen financial inclusion for unbanked populations worldwide. Let us take a closer look by answering some common questions:

Aren’t most payments already digital with debit cards and Venmo accounts?

Considering that most payments already process without the exchange of fiat (paper) money, it is fair to say our currency is already digitized. When we look at the balance in our checking account, we see numbers represented by a series of 0s and 1s behind the scenes. These electronic dollars are only partially backed by reserves under what is known as fractional-reserve banking. The problem with transacting money in this manner is the reliance on banks to serve as intermediaries in cross-border payments, resulting in many unnecessary bottlenecks and expenses in the payment system. Here are some common examples:

· When wire transfers are made between banks without existing relationships, money must flow through intermediary banks, causing slow settlements, processing delays, and higher fees.

· When money is sent from England (GBP) to China (CNY), the currencies would need to be exchanged through a common currency like USD first. This might not be a problem in your daily life, but it shows the deadweight loss taking place in our global economy in one form or another.

· Apps like Venmo still adhere to these same problems since they link to your traditional bank accounts.

Though your dollar might feel digitalized, our banking system is still operating in the same inefficient, private sector-focused manner that it was 50 years ago. In a sense, we have reached the ceiling of the SWIFT banking system, and in our eyes, it is time to make the jump into a fully digitalized financial world.

What exactly is a Central Bank Digital Currency?

As economies continue to develop, our use for cash has been in decline. In short, a CBDC is a fully digital version of a country’s fiat currency that a central bank would issue into circulation. It has the same functions as paper money, including legal tender (universal acceptance), unit of account, medium of exchange, and a store of value. A central bank like the Federal Reserve would still use CBDCs to dictate the monetary supply and hold reserves to back up the currency. To be clear, a CBDC would not fully replace paper money but instead be used as a compliment, much like paper money came to complement metal coins centuries ago. Obviously, transferring your currency onto the internet is more menacing than changing physical objects you can hold. However, think about how less daunting 2020 would have been if you could have had your stimulus money issued directly into your pocket instead of waiting for a direct deposit.

Much like fiat currency, a CBDC would be a public good. Currently, once hard cash is deposited into bank accounts, our whole financial system becomes increasingly privatized. By having the option to store money in a digital wallet (more on these later) held independently from banks, consumers can unlock immediate settlements on transactions with fewer processing delays. This digital currency would have no investment value and be used solely for commercial online payments. CBDCs would also have a profound effect on the unbanked population. According to the National Survey of Unbanked and Underbanked Households, 6.5% of American adults do not have bank accounts due to high deposit fees in checking accounts and minimum balance requirements. Without accessible and affordable financial services, underbanked populations must find alternative means of completing regular financial tasks such as cashing a check or sending money to family. The integration of CBDCs would grant anyone with internet access the ability to send and store money easily.

Though CBDCs are not of immediate importance here in the United States, the concept would increase financial inclusion for many disadvantaged areas around the globe. Countries such as China, Sweden, France, the Philippines, Japan, Turkey, and Switzerland have begun testing their own CBDC with the public; meanwhile, the Bahamas has already launched its CBDC called Sanddollar. CBDCs should be designed with some similarity to create a more financially cohesive world, and for this reason, the United States needs to act fast or it will be playing catch up.

How do Centralized Bank Digital Currencies work?

There are many avenues to explore for the development of CBDCs. We note that the original inspiration for digital dollars came from blockchain technology modeled by Bitcoin. However, it is crucial to distinguish that a CBDC will not take the form of a cryptocurrency like Bitcoin or Ethereum due to the decentralized nature of these blockchains and the expansive computing power required to operate the networks. Instead, we expect CBDCs to model a centralized blockchain like the real-time settlement system Ripple. This form of privatized ledger is only accessible by financial institutions that have the privilege to oversee the network. The centralized blockchain would allow governments to closely monitor a digital system and bring it to scale.

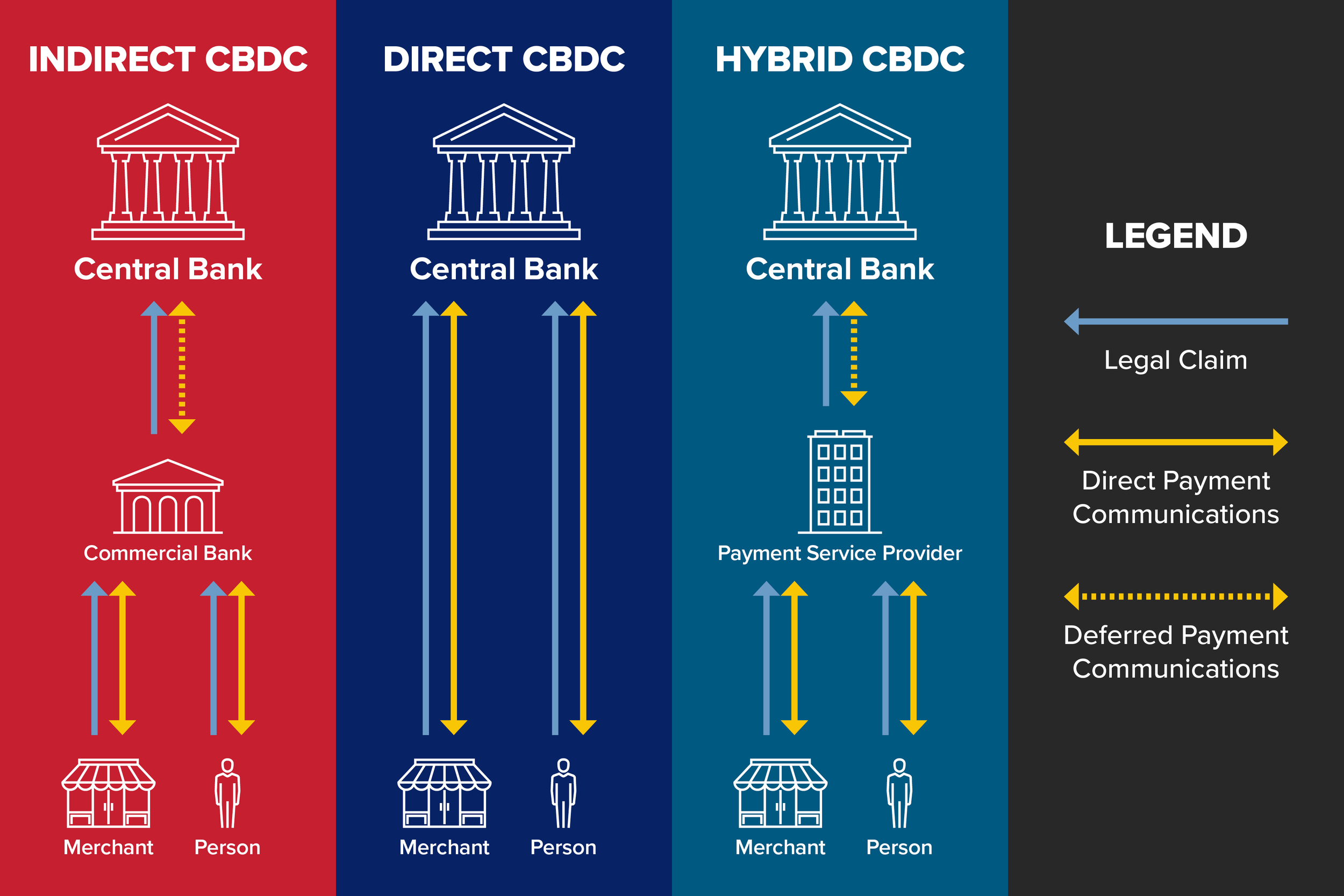

Within the network, CBDCs are being designed as tokens backed by a certificate system with digital signatures to prevent illegal duplication and counterfeiting. These uniquely identifiable tokens will be monitored by a database keeping track of transactions made by people and corporations. The currency will be held in software-based, digital wallets that securely store users’ payment information and are accessible with any internet connection. Once again, CBDCs are the direct liability of a country’s central bank, making it responsible for distributing and overseeing these wallets. For this reason, there are three different approaches for the distribution model:

I. Direct CBDC: The CBDC is a direct claim on the central bank, which keeps real-time records and updates balances. Private sector companies may still develop token-based variants or digital banknotes.

II. Indirect CBDC: The CBDC is indirectly issued by the central bank and represents a claim on an intermediary. Intermediaries handle retail payments while the central bank handles wholesale payments.

III. Hybrid CBDC: A direct claim on the central bank is combined with a private sector messaging layer. Payments are handled by intermediaries. The central bank has the capacity to restore retail payments if intermarries are under technical stress.

If citizens have CBDC accounts held by the central bank in a direct system, commercial banks won’t have much of a role to play anymore. Many would support the disenfranchisement of commercial banking after the role they played in 2008

Note: CBDCs are considered a competitor to stablecoins like Tether. These cryptocurrencies are directly tied to the USD on a 1:1 basis while utilizing the efficiency blockchain technology offers. These coins have become an alternative open payment network. Unlike stablecoins, a US CBDC would be backed by the full faith and credit of the Federal Reserve System.

So, where do we stand today?

The United States Federal Reserve is currently running behind its major counterparts: the European Central Bank, the Bank of Japan, and the Bank of England (which has led CBDC research over the last half-decade). Federal Reserve Chairman Jerome Powell stated that a CBDC is a high-priority project, but we haven’t heard of progress since the G20 summit in July. Behind the scenes, we know that US research is being spearheaded by MIT and the Federal Reserve Bank of Boston, along with The Digital Dollar Foundation and Accenture. These two projects are worth keeping an eye on as they develop pilot programs in the near future.

On Wednesday, G7 officials stated "We reaffirm that any CBDC should be grounded in our long-standing public commitments to transparency, the rule of law and sound economic governance. Any CBDC must support, and ‘do no harm’ to, the ability of central banks to fulfill their mandates for monetary and financial stability." Meanwhile, the Bank of Japan has announced a simple CBDC design where the digital yen will be vertically integrated within the private sector to incentivize the CBDC’s adoption. Ultimately, Japan hopes to compete with China’s digital yuan on the international stage.

The inevitable introduction of Central Bank Digital Currencies (CBDCs) could be the most historic and fundamental change to the global financial system since Bretton Woods. In almost any iteration, they have the potential to change the face of finance, and ultimately, change the nature of money itself. Through CBDCs, fiat money will become truly digitalized and finalize the merger between monetary and fiscal policy. Therefore, we highly encourage our readers to research further and educate themselves on the topic. Should central bank digital currencies be developed or introduced in any magnitude, we must acknowledge our financial system to be evolving. All concepts, from how credit is created, the role of central banks in society, monetary and fiscal policy transmission mechanisms, how transactions are processed, and who is included in the economy, have the potential to be redefined and re-engineered entirely.